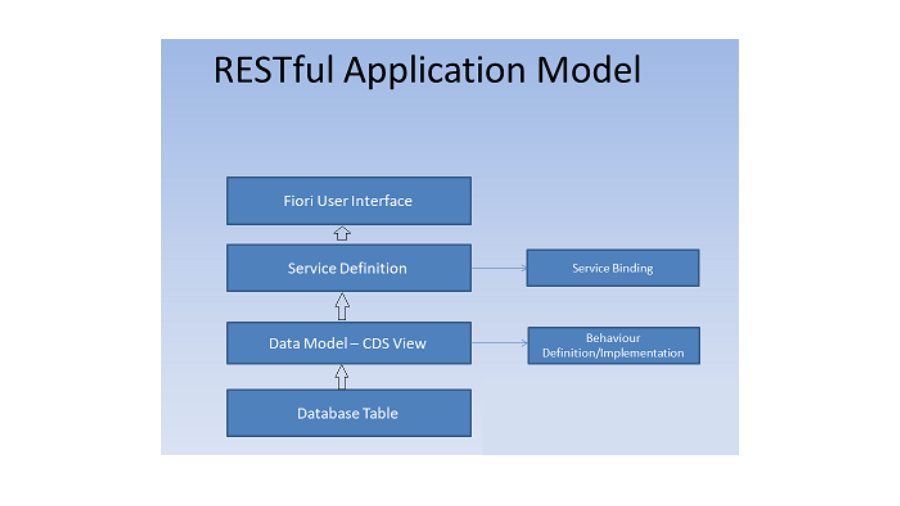

As an answer draftsman, is it expected to make a conduct definition and execution for all rundown reports? Is conduct definition just an answer for make a rundown report? Well No! Unmanaged Query in RAP.

We have frequently known about Unmanaged Query in RAP conduct that we want to perform Muck procedure on, however unmanaged inquiry is rarely heard and considered. Well it is a secret gem in RAP world where in the event that we need to zero in on just Understood activity and a rundown report where determination is the principal rules, this ought to be an able decision.

All in all, assuming that the questioner asks you, When should Unmanaged Question be picked? You have the instant response above. Remember it.

Compact discs Custom Substances are composed where Cds usefulness isn’t adequate for information determination. It tends to be connected with a model where the information requires a Programming interface or a capability module to be called where the information can’t be straightforwardly separated from the information source.

The majority of us are in a deception that the RAP is just accessible in the cloud, while it begins from S/4HANA 1909 variant. One more inquiry question for you.

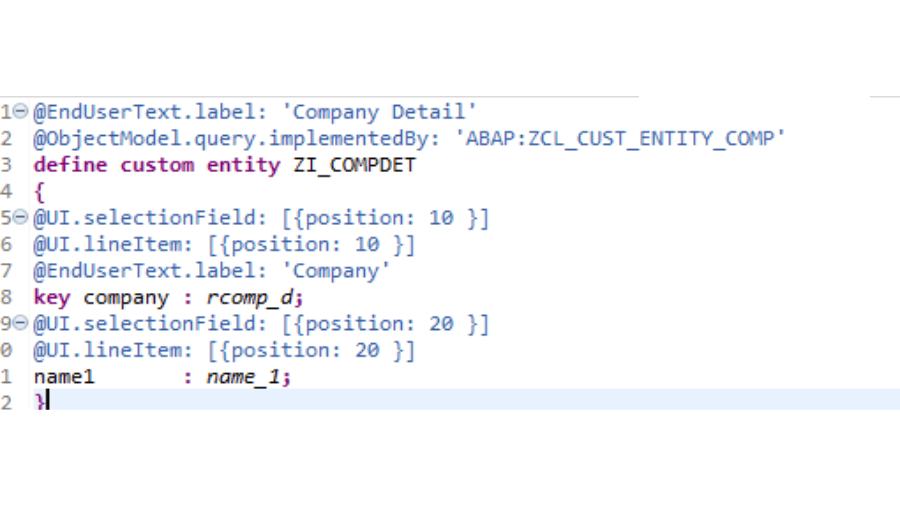

These are accessible from ABAP discharge 7.55. The runtime is executed by ABAP Class. The custom Cds substance doesn’t have a SELECT assertion and the runtime is executed by adding the comment @ObjectModel.query.implementedBy.

Trigger a Workflow to Send an Email Whenever a Material is Created

Let’s get it created with Unmanaged Query in RAP.

Create a Custom CDS Entity

Implement the Class

Execute the class ZCL_CUST_ENTITY_COMP: The ABAP code can be carried out in the strategy for the connection point if_rap_query_provider. This connection point has just a single technique Select. The boundaries of the technique are io_request and io_response which is the groundwork of the client-server engineering of HTTP convention. The paging and the channel can undoubtedly be gotten from the io_request.

Trust the code is more clear!

When the class is made, one generally attempts to execute the Cds View to check in the event that information is getting showed (as adjusted by the propensity for a designer) . In any case, the custom Compact discs elements are not executed.

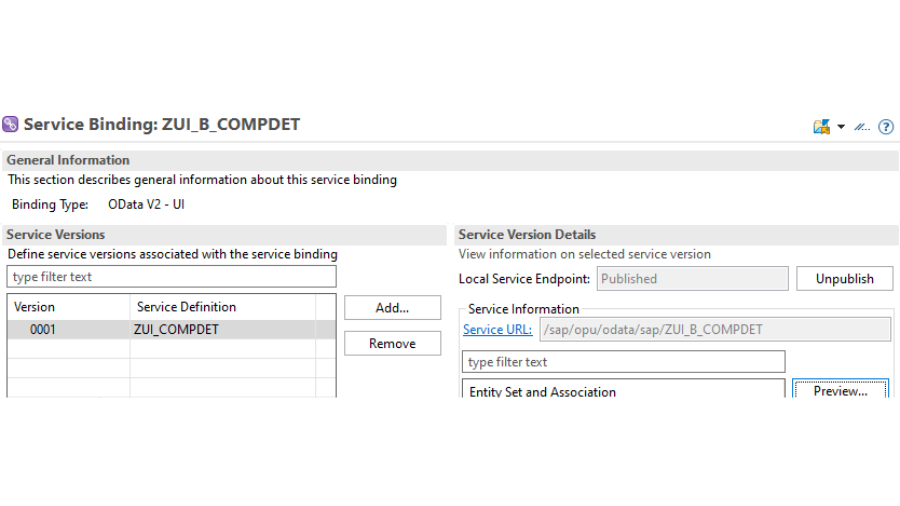

Create Service Binding

Following stage is to make the Service Binding. Right snap on the help definition and make the assistance restricting. Distribute the assistance and see it.

Performance Optimization in ABAP on HANA: Uniting CDS and AMDP

Preview the Output

Select the element and snap on review, the outcome is very much shown.

Select the component and snap on survey, the result is especially shown.

Trust, another component for Soothing ABAP programming model is substantially more fascinating and helps with contriving amazing arrangements!

Elevate Your Conversations with SAP BTP SAP Conversational AI! Unleash the power of seamless communication and automation within your business processes. Explore the synergy of SAP Business Technology Platform (BTP) and Conversational AI for a transformative digital experience. Learn more about the future of intelligent conversations

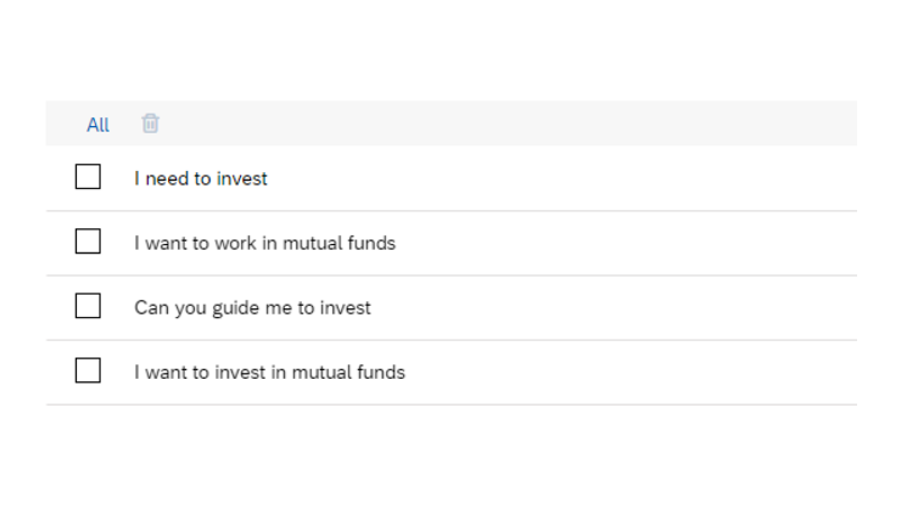

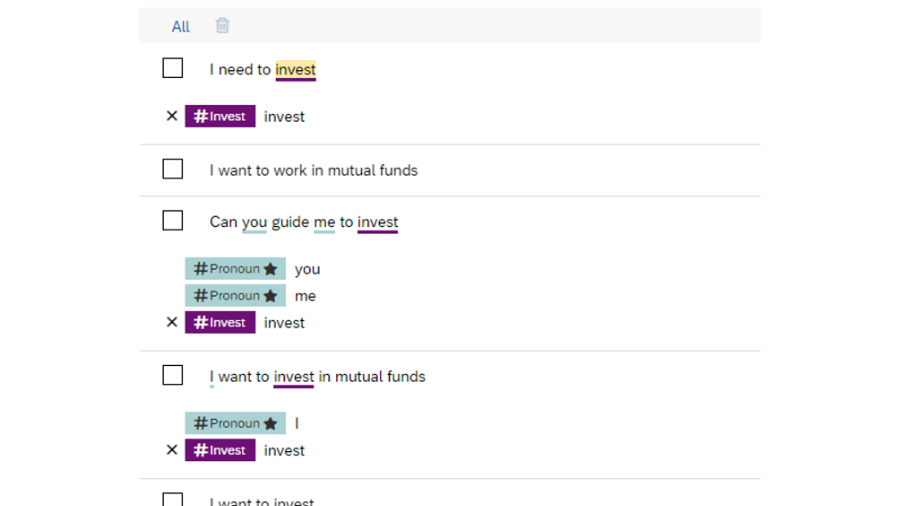

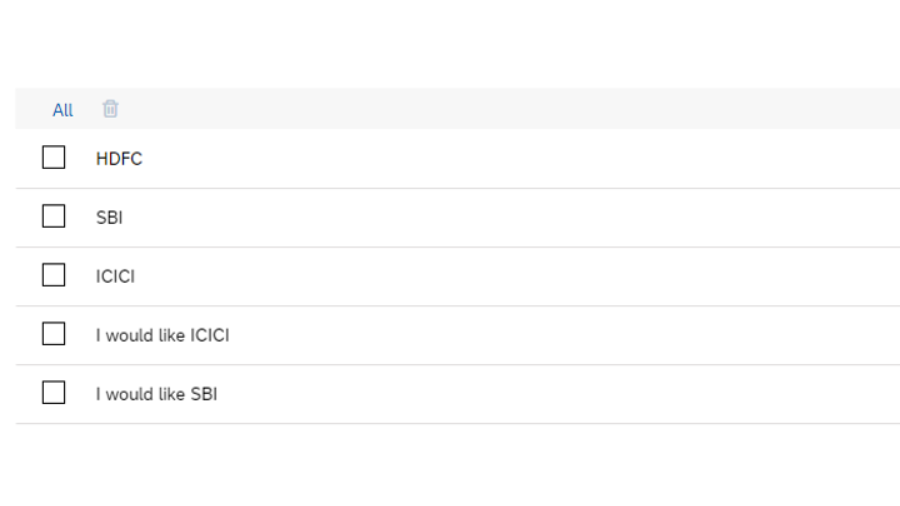

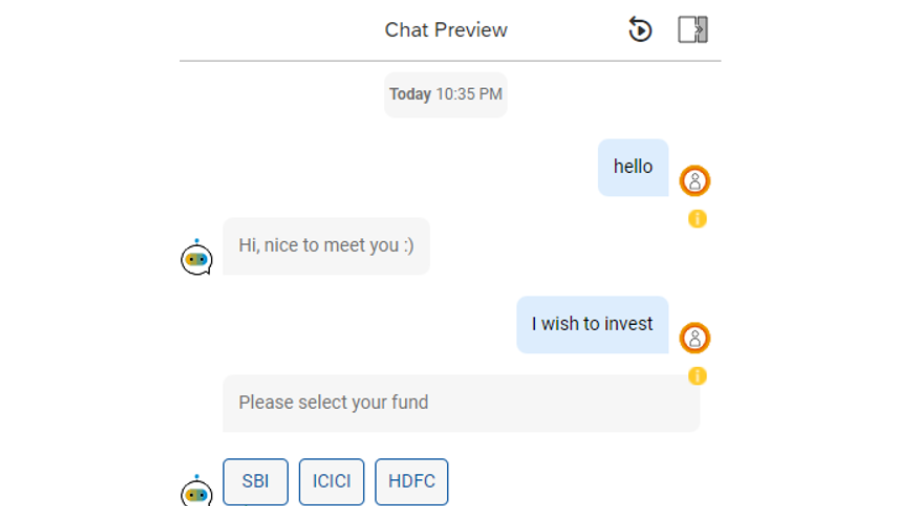

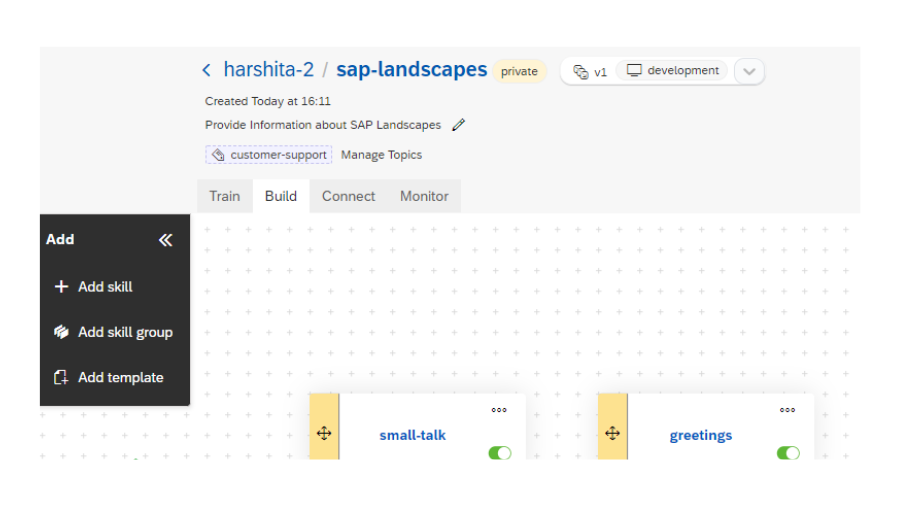

Make a bot, I have named it as mutual funds and added casual banter and hello abilities.

Make an expectation @invest – This plan is liable for the main client input, when the client starts a solicitation to contribute. To explain client input, we have made articulations.

I have added below expressions.

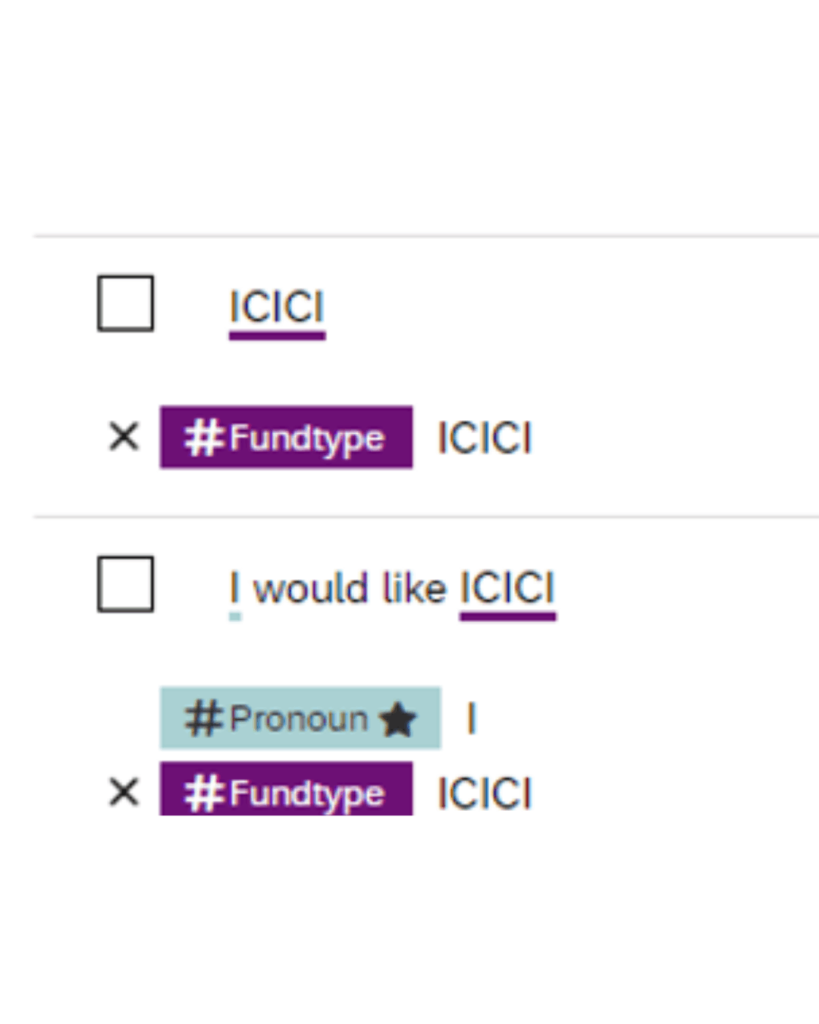

3. Make a restricted entity, #Invest. This substance is mindful to find the word put resources into an expectation. In the event that a sentence contains the word contribute, it will direct to contribute aim. The articulations in the goal are then related to the element #invest. SAP BTP SAP Conversational AI.

4. Make another intent @mutualfund. This expectation is liable for the client input about the particular common asset he wishes to contribute. The articulations are the kind of assets which the bot anticipates from the client.

SAP BTP: Decoding the Business Technology Platform

5. Make confined substance #Fundtype. This substance distinguishes the asset name in a given articulation.

It is time to train the bot.

6. Make an expertise called invest.

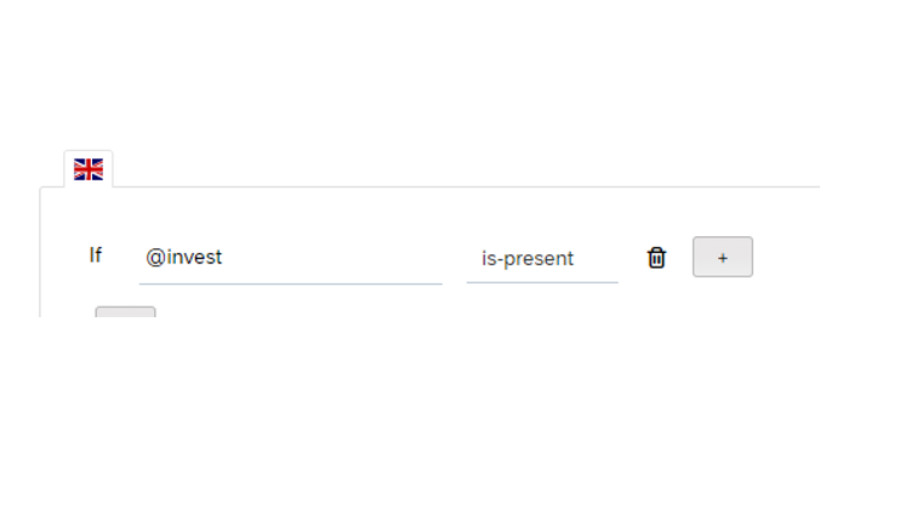

7. The trigger of this skill would be that intent @Invest should be present.

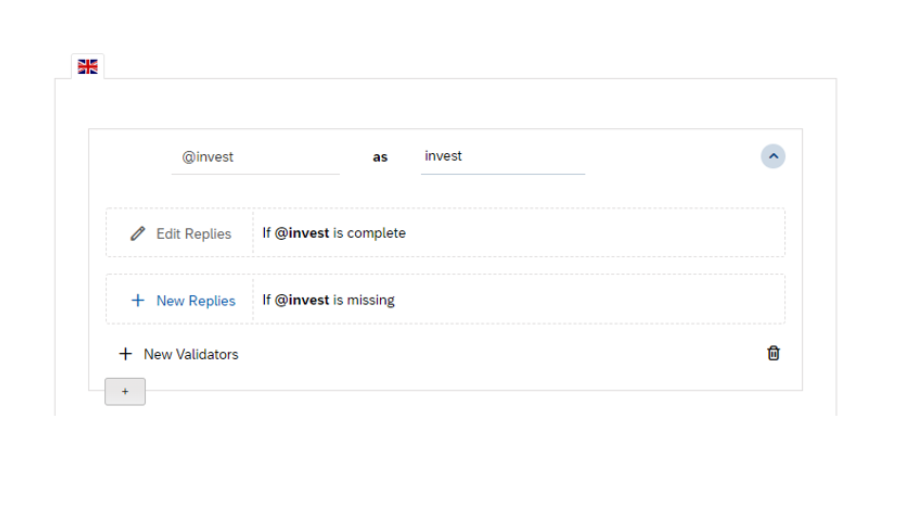

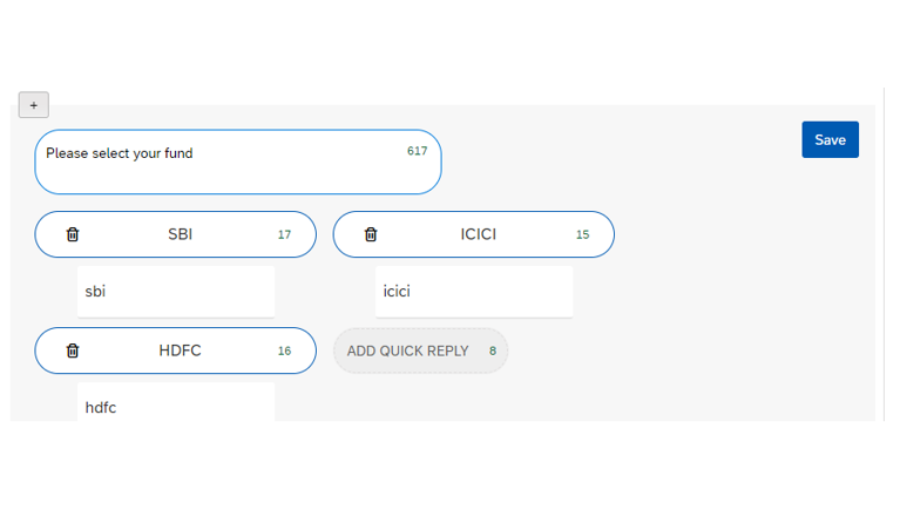

8. In the necessities tab, we have composed if @invest as contribute, that is on the off chance that contribute is finished, implies in the event that the client has entered that he wishes to contribute. We add a message as type fast answers.

9. We have added quick replies are SBI, ICIC and HDFC.

Press save.

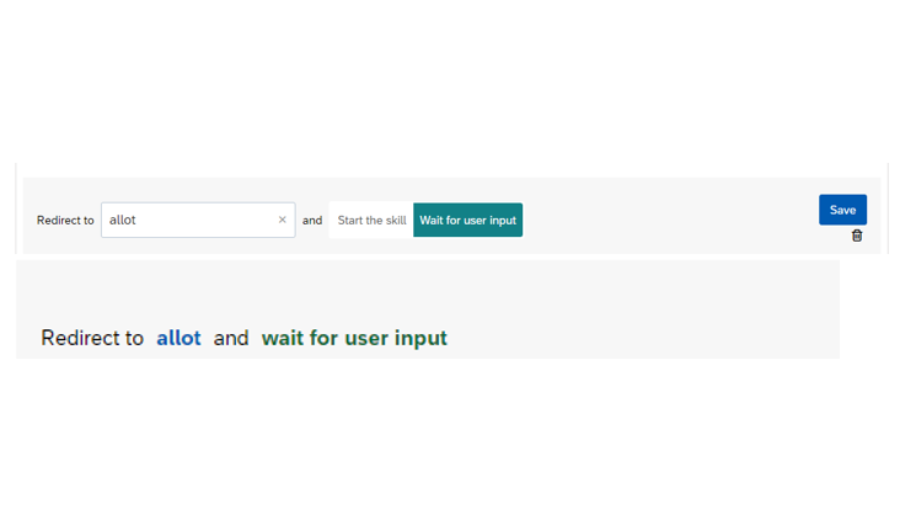

10. In the activity tab – Snap on update discussion and snap on GO TO.

11. Write divert to assign expertise and hang tight for client input.

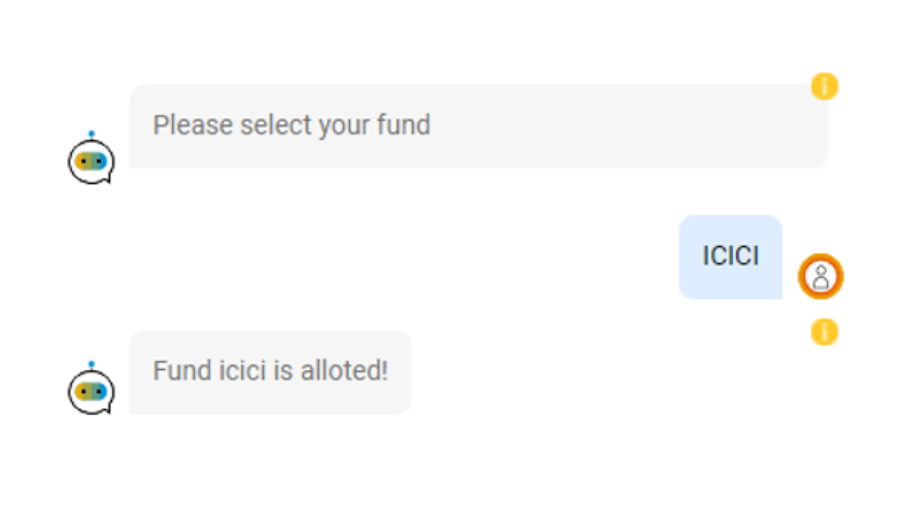

12. Prior to this step, make one more expertise as allocate. When we present to the client the assets, we would sit tight for the client input and would divert to expertise allocate.

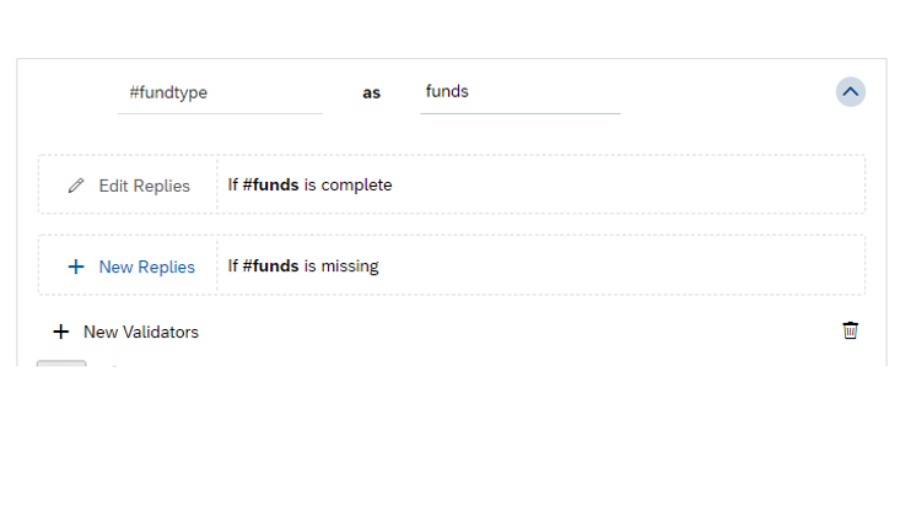

13. The trigger of the distribute expertise is check if plan @mutualfund is available that is assuming the client has entered the asset type.

14. In the requirement tab, we would check if specifically the entity #fundtype is present. Click on new replies for If #funds is complete.

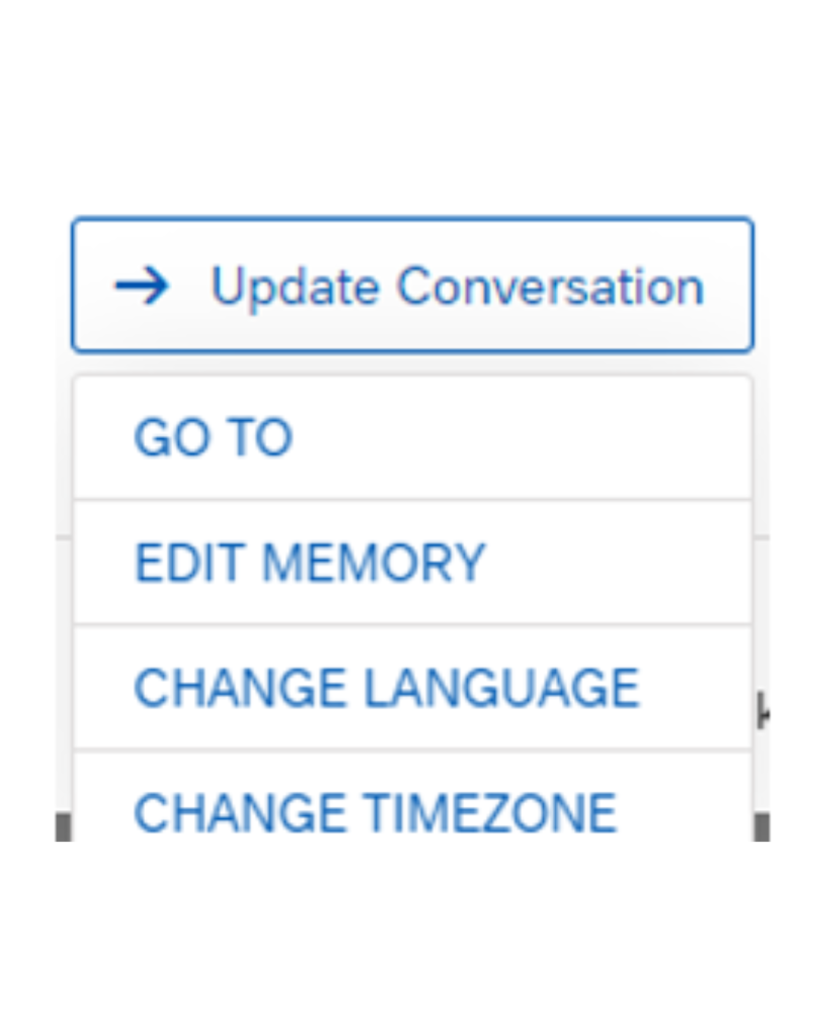

Click on update conversation – edit memory.

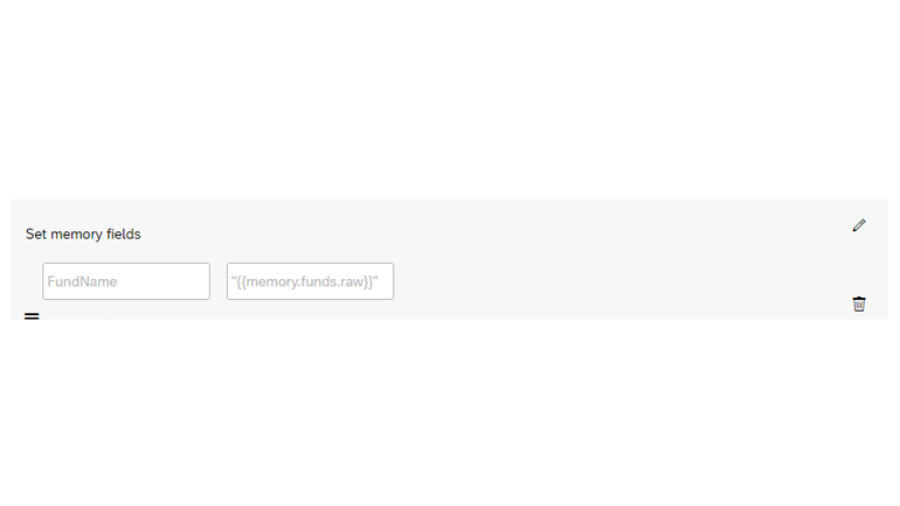

Set memory fields and store the user input in the memory. In this, in variable FundName, we have assigned from memory i.e. “{{memory.funds.raw}}” .It will get the value of the entity type.

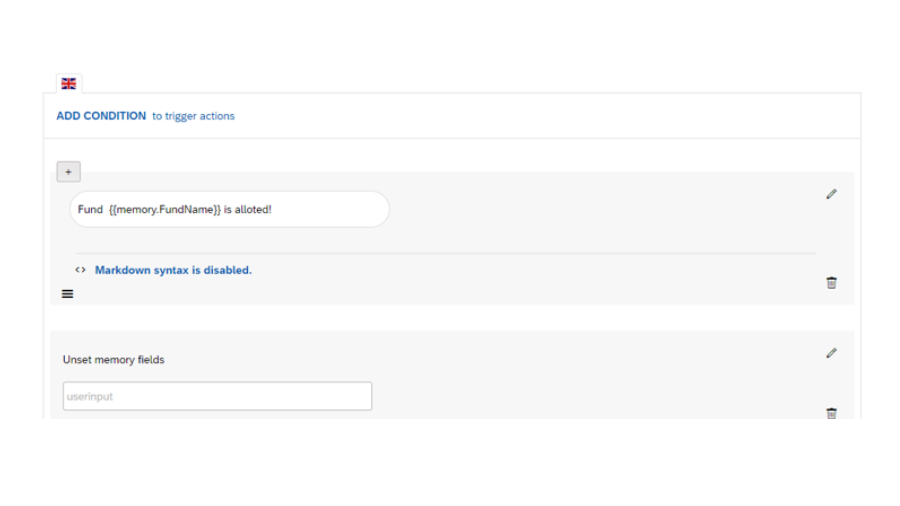

In the Activities, Compose message as message Asset {{memory.FundName}} is alloted! The memory variable will be tended to as the variable in which memory was put away. Then, at that point, click on update discussion – >edit memory->unset memory fields. This is utilized to unset the client input, very much like clear articulation in abap.

Hope the design is fine. Train the bot and test it.

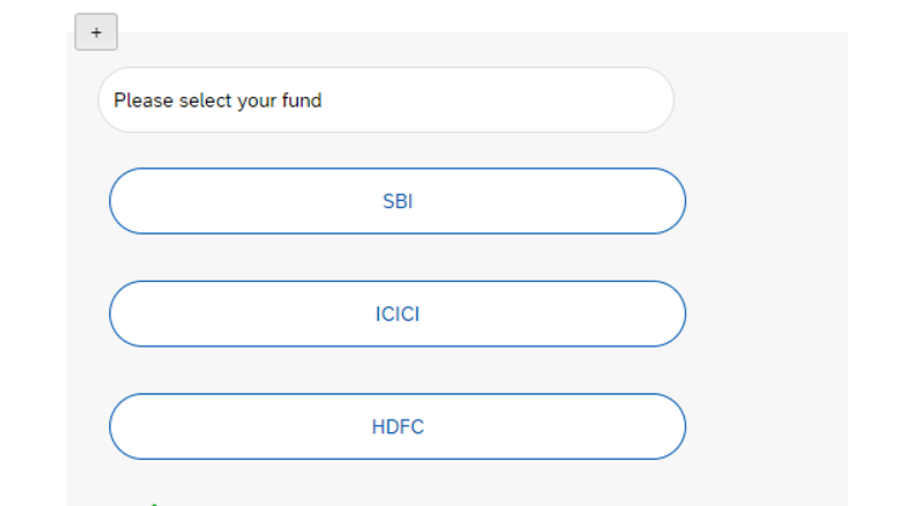

In the principal explanation ability good tidings is set off. In the subsequent one, ability put is set off in which the client has wanted to contribute and the plan @invest is distinguished by the bot. Consequently as this necessity is satisfied, the bot has asked fast answers from the client. The client can choose one of the buttons.

As client chooses one of the buttons, the expertise dispense is diverted and the bot checks if the purpose @mutualfund and substance #fundtype is found, the memory is caught and the activity text is set off!

All things considered, for certain new presentations as update_conversation, A bot is given an out and out another usefulness. Might we at any point additionally request that the client enter the sum to contribute and call an odata administration to store the asset and the sum! Remain tuned!

Artificial Intelligence: It is one of the most well-known phenomenons that maybe every single arising innovation needs to implant in. We as a whole have known about Alexa, Siri and so forth intuitive robots to help clients and these have arisen as venturing stones in the separate innovations. SAP Conversational AI.

Consequently, moving inseparably with innovation SAP has previously presented Conversational Man-made brainpower which is SAP Conversational AI. It is a strong computerized colleague intended for the association.

Artificial Intelligence: A Concept

As properly described by the actual point it is a strong bot building stage that helps you fabricate and convey conversational specialists in your application. These specialists are the automatically planned mechanical specialist that collaborate with the end client and gives a strong end client cooperation. It gives a web UI that fills in as a stage to make, construct and test visit bots. It is for sure computerization.

However SAP has effectively made splendid and easy to understand UIs with hearty Fiori applications and inserting them with conversational points of interaction demonstrated cherry on the cake. This has smoothed out to a much better and smoother client experience. Brilliant talk bots permit client to get quick and directional reactions to their inquiries about a specific applications. They are significantly more brilliant to welcome clients as though a genuine specialist would go to them. SAP Conversational AI.

is SAP Consultant a good career ?

What are chat Bots?

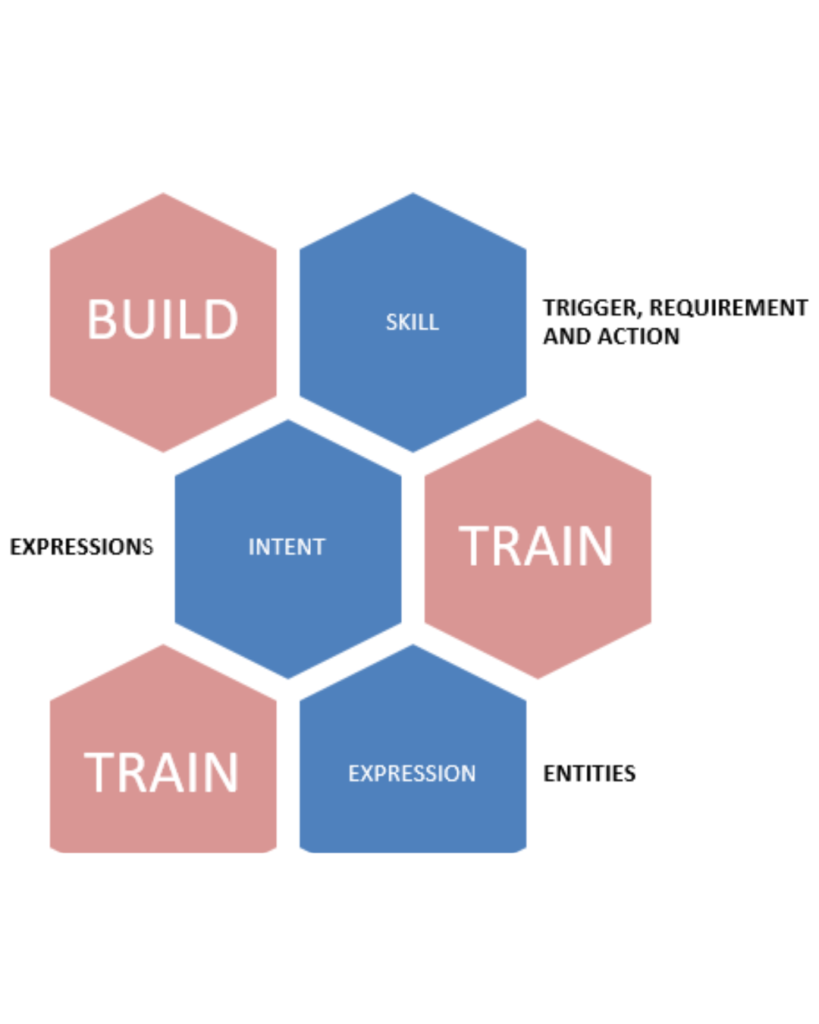

A chat bot is a robotized window or a connection point intended to collaborate with the end client. They are intended to recreate human discussion with the end client. A Visit bot mechanizes the business cycle and further develops client care. There are a few rudiments connected to the visit bot. A visit bot is made out of the beneath essential components:

Expertise: An ability is the reason for which a talk bot is intended for to accomplish an outcome. For instance, plain good tidings, checking climate projection, executing a little undertaking and so on. Preparing Informational index: It is made out of the possible smart sentences that the client would use in his essential discussion in a bot. It likewise stores the changed sentences that contain a comparative importance.

Articulations: The sentences that client can request to interface with a visit bot is known as articulations. It tends to be a Straightforward ‘Greetings’, or a sentence requesting some help. Expectation: The arrangement of articulations that are built contrastingly however implies exactly the same thing is supposed to be plan. In light of any articulation, not set in stone and is correspondingly answered. Element: A Substance is the event of the catchphrase that most likely figures out which aim should be set off.

Trigger: A bot comprise of numerous abilities clubbed together and a Trigger is a condition that figures out which aim the bot will execute. Necessities: The data that an expertise gathers to play out an activity. Activity: Activity is at long last the step the visit bot will perform or execute upon a client’s solicitation. The above focuses could sound interesting yet they are exceptionally simple to carry out!

Is there AI for SAP?

AN OVERALL MODEL OF A BOT

An Example of a BOT – A Simple digital Assistance!

Training a Chat Bot:

We will rapidly perceive how to make a basic talk bot as above.

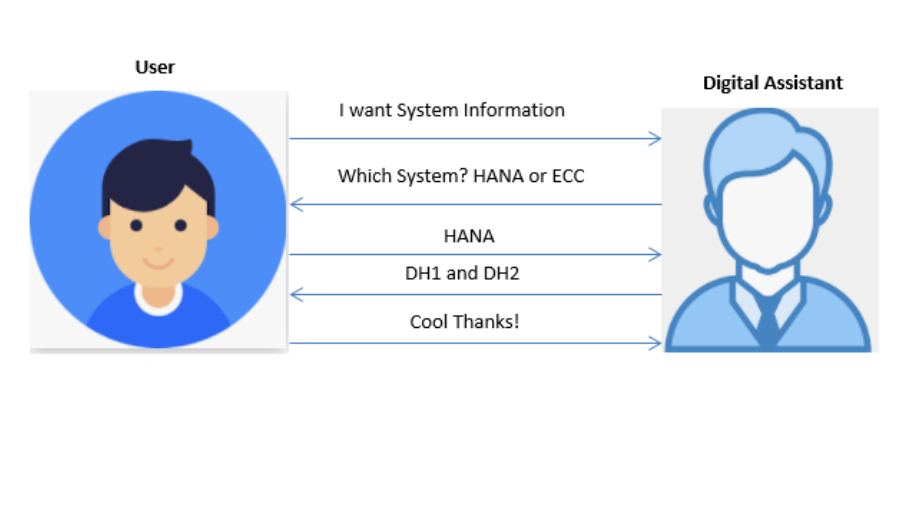

Reason: This talk bot will tell the client the different scene of SAP frameworks.

We visit the SAP Conversational AI platform and register an account.

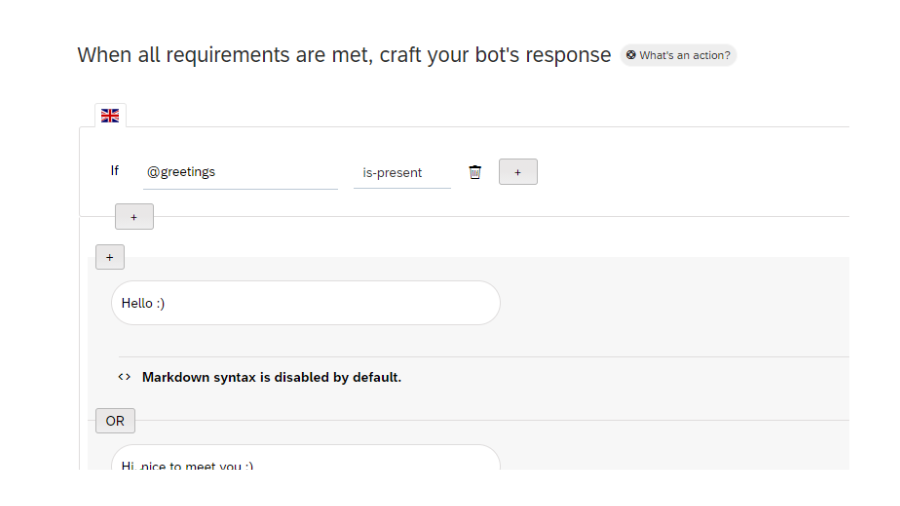

We click in New Bot. When we click here, we select that our visit bot will perform activities and select a given expertise. We select good tidings and casual banter. Good tidings and casual banter is the standard abilities having its own aims and triggers.

We give a name to the chat bot, its purpose.

We give the information strategy according to security reasons. It shows that the visit bot are gotten as well.

Select the visibility of the bot and create the bot.

We land to a page where we need to give purpose to the visit bot. As we have chosen abilities as Good tidings and casual chitchat, so our most memorable expectation would be articulations connected with good tidings.

Sap has already provided some pre build skills in which @greetings is one of them.

Assuming we select form, we are given two abilities that we have chosen for our visit bots.

These are:1) Small-talk 2) Greetings

We can add more abilities here as well. Assuming we discuss good tidings, every one of the ideas that we read before are obviously noticeable:

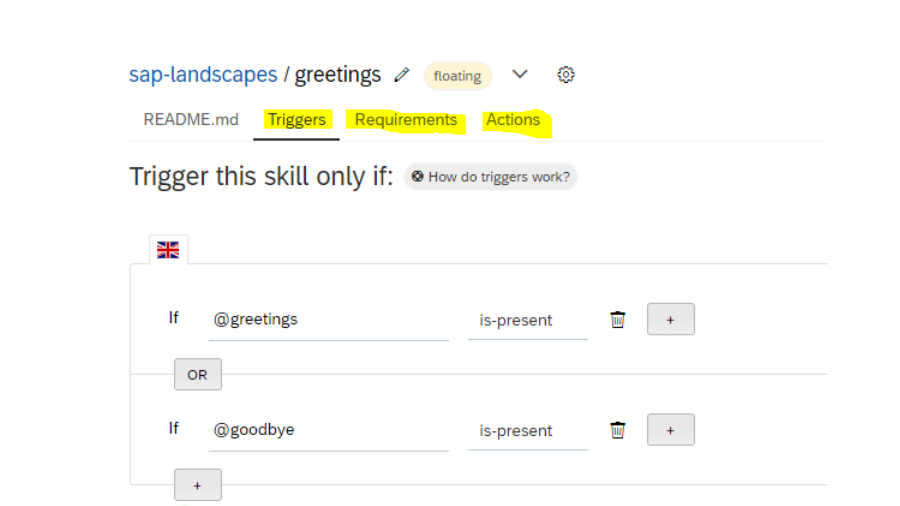

Triggers : When user greets the chat bot that will be the trigger point. Requirements: There is no requirement as such here. Actions : Once the trigger is executed, the actions are performed which in this case is greeting the user back. We can also edit these messages.

In the past series we examined about the essentials of BTP and how the programming worldview has been changed in the RAP advancement. Presently it is the ideal opportunity for the practicals! Allow us to foster our most memorable essential straightforward RAP Application. Managed RAP Scenarios.

However presently there have been many articles in which a RAP model is depicted, but this article manages the reasonable stumbles we as a whole would commit while creating one!

The article floats around oversaw conduct of a RAP Application. At the point when it is a straightforward application and you need to pass on the rest to Drain, Oversaw is the best one for you.

Managed RAP ScenariosPractical Time !

So I entred my ABAP Cloud project and added the most loved bundle. This step is a custom at this point!

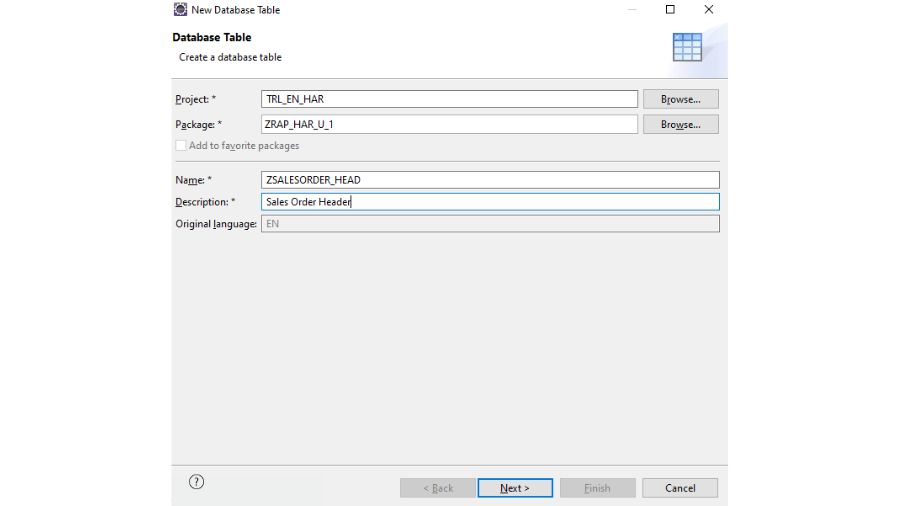

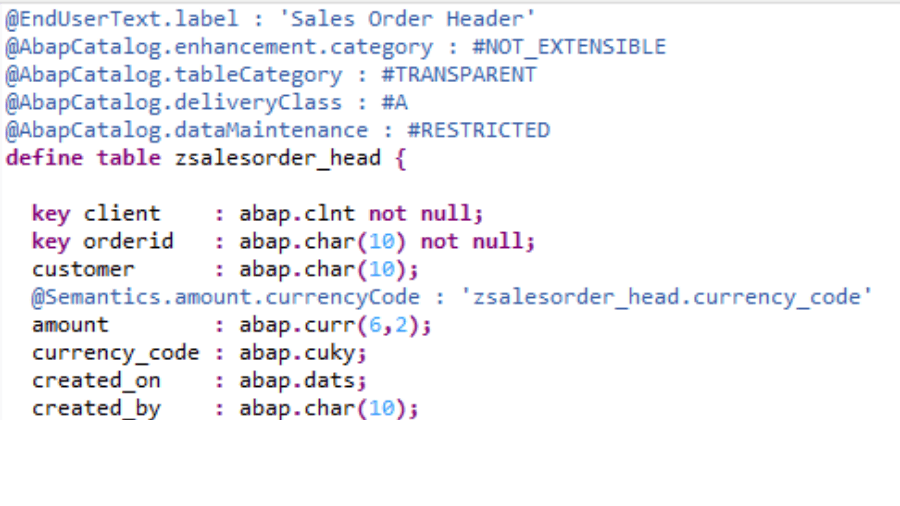

Step1 – The base is always a database table. Why should I always sail across the flight tables, thus I created an Order table which would relate to the not so forgotten traditional SAP.

Dictionary->New->Database Table

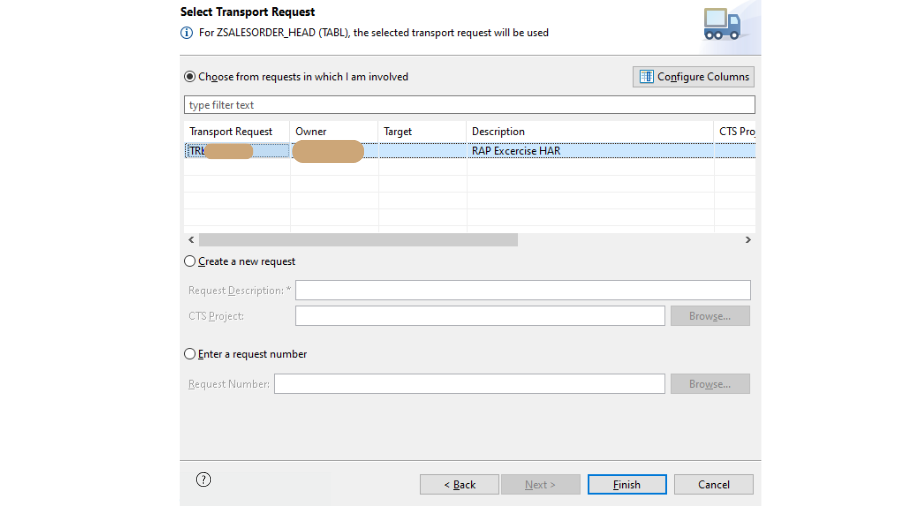

Select a transport request

The old fashioned fields have been made in the table. However we are altering in ADT, remember to make reference to the Sum money fields.

Indeed, presently the table has been made, I might want to embed not many records in that frame of mind through a class.

By the way, can I create a report in the cloud as well? Is there any ways to know which objects are supported on cloud? Well Yes!

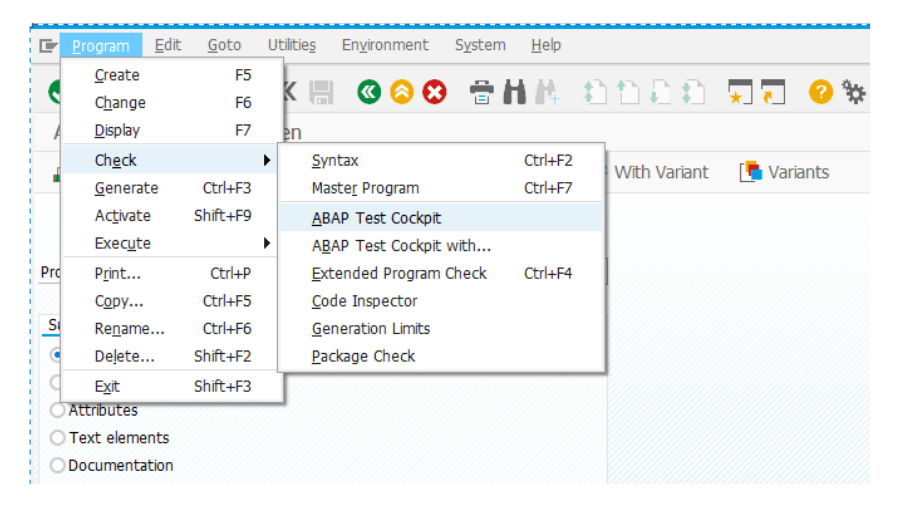

In the GUI Framework, I made a report and checked through ABAP Test Cockpit with…

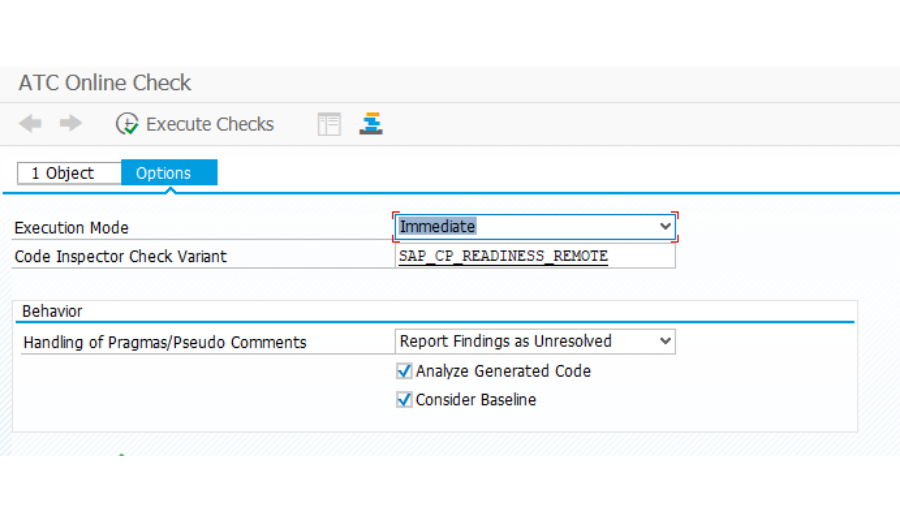

In the choices, give a variation SAP_CP_READINESS_REMOTE. Besides, we can default the variation in the tcode ATC. In the way of behaving, actually take a look at the choices as displayed in the screenshot.

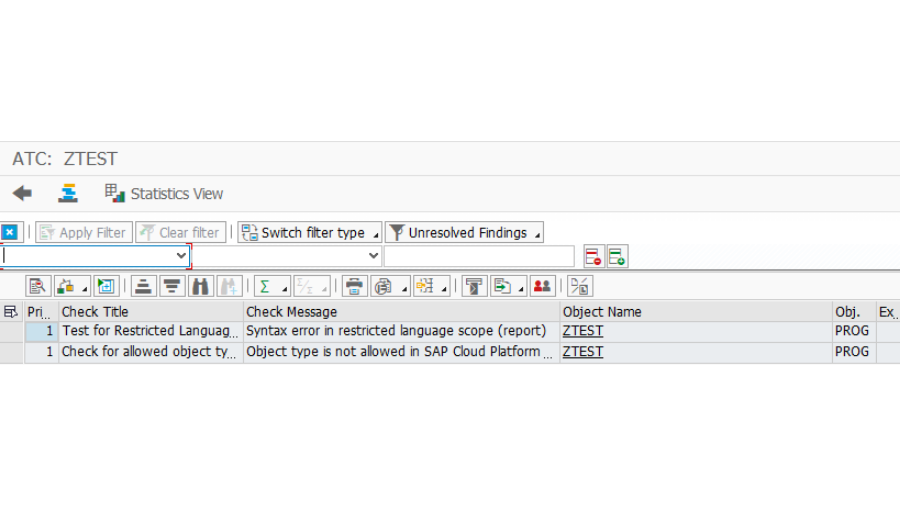

After executing, we would get the below findings, object type report is not allowed in cloud.

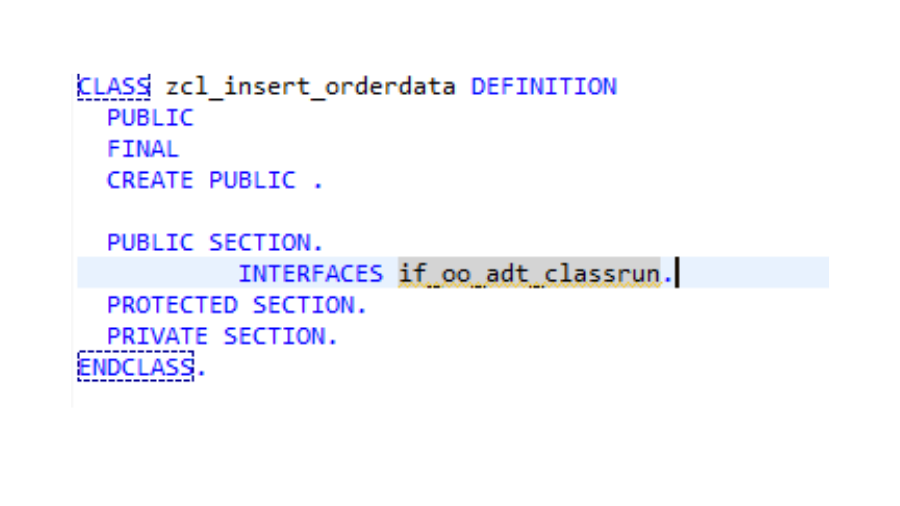

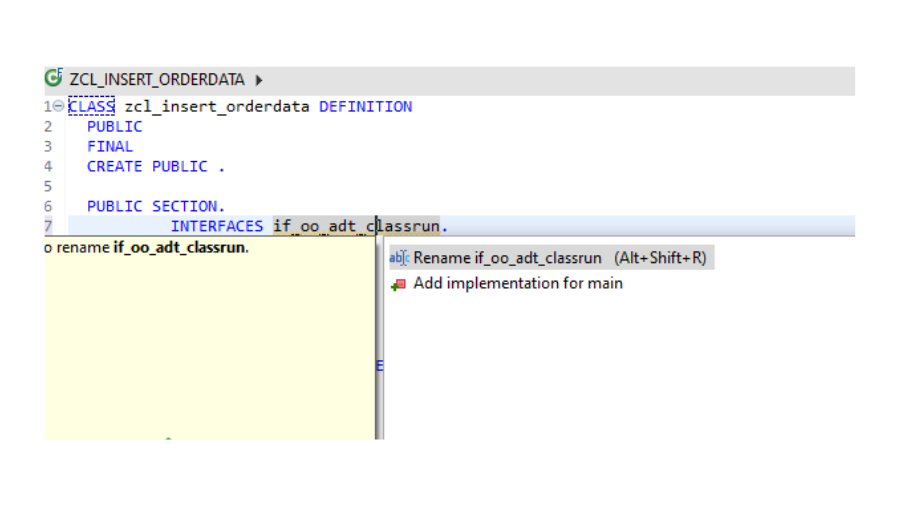

So the people who are still miles from ABAP OOP, lock in, this is the best way to code in the cloud. In this way, we made a class with a connection point if_oo_adt_classrun. This connection point is utilized to test the result in support like reports?

For executing the strategy principal in the connection point, I made an easy route. Ctrl 1 which would recommend adding the execution to the connection point.

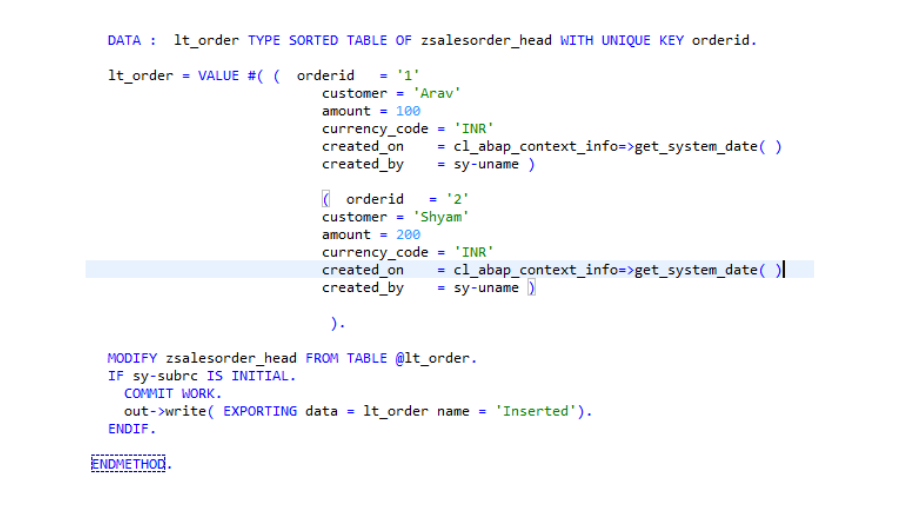

However I have utilized the old procedure to add the information in the table, by and by the new strategy is now thumping the entryway.

Thus I turned the pages and ran the report ABAP_DOCU_VERSION_WHITELIST in on-premise system.

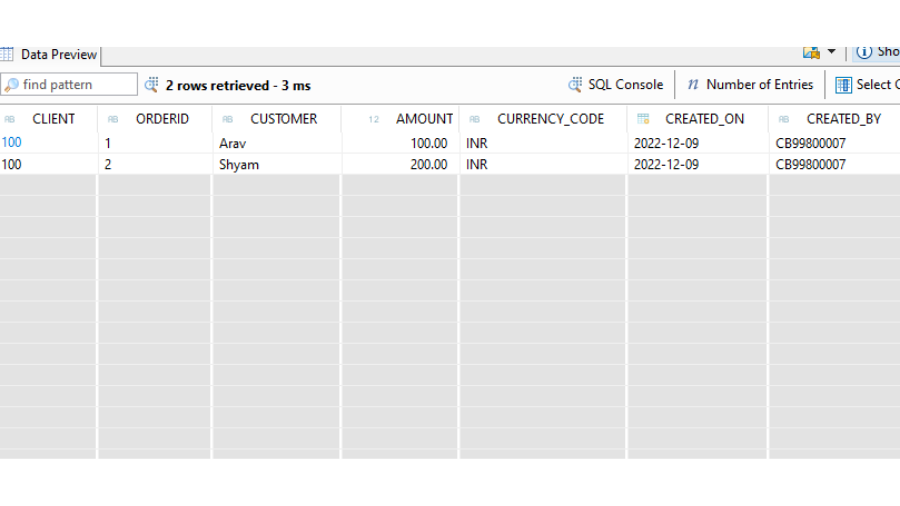

I can view the output in the console and also when I execute the table data.

The improvement isn’t done at this point. Look at the primary kinds of RAP in our next article.

In the past series we examined about the essentials of BTP and how the programming worldview has been changed in the RAP advancement. Presently it is the ideal opportunity for the practicals! Allow us to foster our most memorable essential straightforward RAP Application. Managed RAP Scenarios.

However presently there have been many articles in which a RAP model is depicted, but this article manages the reasonable stumbles we as a whole would commit while creating one!

The article floats around oversaw conduct of a RAP Application. At the point when it is a straightforward application and you need to pass on the rest to Drain, Oversaw is the best one for you.

Managed RAP ScenariosPractical Time !

So I entred my ABAP Cloud project and added the most loved bundle. This step is a custom at this point!

Step1 – The base is always a database table. Why should I always sail across the flight tables, thus I created an Order table which would relate to the not so forgotten traditional SAP.

Dictionary->New->Database Table

Select a transport request

The old fashioned fields have been made in the table. However we are altering in ADT, remember to make reference to the Sum money fields.

Indeed, presently the table has been made, I might want to embed not many records in that frame of mind through a class.

By the way, can I create a report in the cloud as well? Is there any ways to know which objects are supported on cloud? Well Yes!

In the GUI Framework, I made a report and checked through ABAP Test Cockpit with…

In the choices, give a variation SAP_CP_READINESS_REMOTE. Besides, we can default the variation in the tcode ATC. In the way of behaving, actually take a look at the choices as displayed in the screenshot.

After executing, we would get the below findings, object type report is not allowed in cloud.

So the people who are still miles from ABAP OOP, lock in, this is the best way to code in the cloud. In this way, we made a class with a connection point if_oo_adt_classrun. This connection point is utilized to test the result in support like reports?

For executing the strategy principal in the connection point, I made an easy route. Ctrl 1 which would recommend adding the execution to the connection point.

However I have utilized the old procedure to add the information in the table, by and by the new strategy is now thumping the entryway.

Thus I turned the pages and ran the report ABAP_DOCU_VERSION_WHITELIST in on-premise system.

I can view the output in the console and also when I execute the table data.

The improvement isn’t done at this point. Look at the primary kinds of RAP in our next article.

Navigating the Cloud with SAP BTP ABAP Environment. ABAP Programming language is prepared to send off in Cloud. As talked about in our past article, we have proactively gone into the BTP Space, really look at this first Decoding the Business Technology Platform Part 1

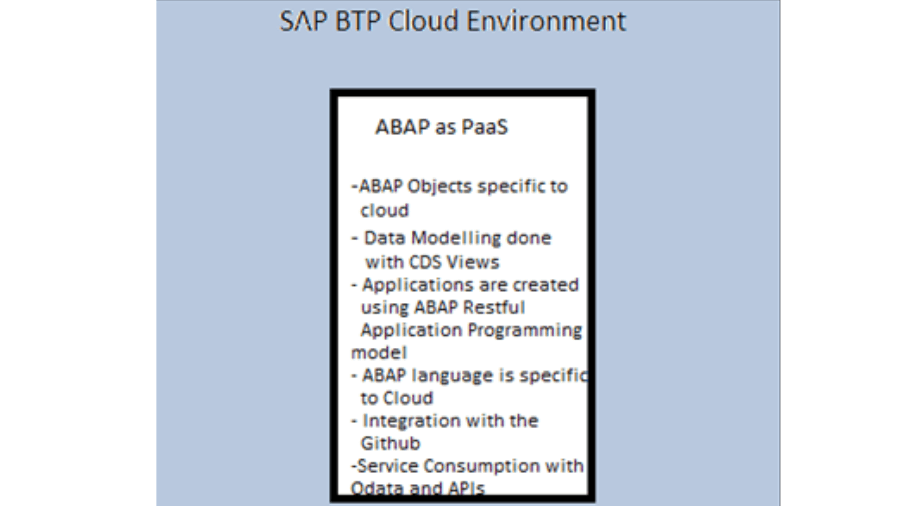

To kick the engine, BTP ABAP Climate otherwise known as Steampunk is utilized to foster applications on Cloud utilizing a Peaceful Programming model. Steampunk is implanted in the cloud climate and the ABAP improvement apparatus utilized is Obscuration where advancement freedoms and organization is overseen by BTP Cockpit.

Steampunk is used as a Platform as a Service which provides a platform for the application development. SAP BTP ABAP Environment.

Important points while using the SAP BTP ABAP Environment:

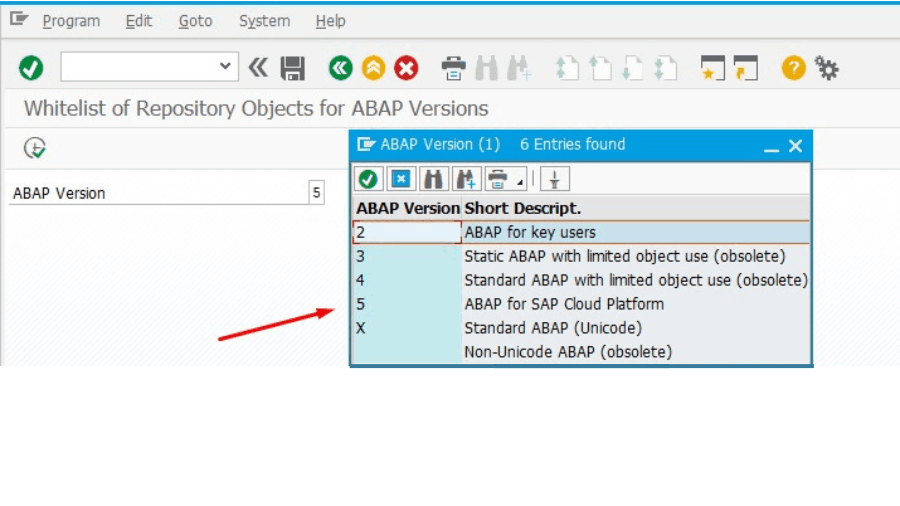

Just Whitelisted ABAP Items are accessible in the Cloud.

These whitelisted items can be recovered involving program ABAP_DOCU_VERSION_WHITELIST with ABAP Form as 5 for example ABAP for SAP Cloud Stage.

Information Demonstrating is finished with the assistance of Discs Perspectives and Albums Substances.

Applications are created utilizing the REST Programming Model.

The ABAP Cloud Language is cloud explicit that is a similar language in on-premise framework might deliver sentence structure mistakes in Cloud.

It has coordination with the GITHUB.

The Administrations depend on the utilization of an Internet Programming interface or ODATA Administrations.

We as a whole are very much familiar with the ABAP programming model in on-premise frameworks that incorporates programs, reports, Odata Model with project creation through SEGW, but in Cloud we follow RESTful Programming Model.

The term centers around the word REST that is Illustrative Condition of the Help. In layman language the information is uncovered as substances dissimilar to the Cleanser Design.

However the Cloud Application Programming model is different yet it is most certainly a condition of-workmanship in the most recent innovations and hence has been at the very front of SAP developments!

They say Money is the Core of SAP, however we engineers accept ABAP is the Spirit of SAP. With ABAP Climate in BTP, the spirit tracked down the glorious home.

In the vast realm of SAP technologies, the term “SAP BTP” has been buzzing around, leaving many ABAP Developers and SAP Consultants scratching their heads. With SAP’s penchant for rapid nomenclature changes and innovations, the confusion surrounding BTP has created a cloud of uncertainty. In this blog series, we embark on a journey to demystify and unravel the wonders of SAP’s Business Technology Platform, catering not only to ABAP Developers but to all enthusiasts eager to grasp its essence.

SAP BTP Unveiled: Business Technology Platform, abbreviated as BTP, is essentially the SAP Cloud Platform rebranded. The introduction of SAP BTP took place in 2020, and a significant shift occurred in 2021 when SAP opted to submerge the name SAP Cloud Platform, giving rise to the brand name SAP BTP.

Steampunk: Powering ABAP Developers:

Enter the intriguing term “Steampunk” into SAP’s dictionary—a name that resonates with power and innovation. Steampunk in the SAP realm specifically refers to SAP BTP ABAP Environment. The term itself, derived from retrofuturistic science fiction, symbolizes the Power of Steam. In essence, SAP coined this name to empower ABAP Developers, infusing creativity and vigor into their endeavors.

SAP Training Offerings in BTP: Delving into the offerings of SAP BTP, three main components take center stage:

IaaS (Infrastructure as a Service): The cloud manages storage, computing, and networking infrastructure, alleviating concerns for users.

PaaS (Platform as a Service): A platform for developing and deploying customized solutions without worrying about storage or infrastructure.

SaaS (Software as a Service): SAP BTP provides on-demand cloud-based applications like SAP Ariba, FieldGlass, SAP Success Factors, SAC, and more.

In essence, SAP BTP is a fusion of Application Development, Integration, and Solutions, seasoned with Cost Efficiency, Scalability, and Optimum Maintenance.

| SAP BTP Certification |

Key Focus Areas: Application Development in SAP BTP centers around Steampunk, incorporating the Restful Programming Model (to be discussed in later blogs) and CAP (Cloud Application Programming) supported by Fiori as the User Interface.

Integration capabilities are finely honed to seamlessly integrate SAP and non-SAP solutions, both on-premise and on the cloud. Common tools include API Management and Cloud Platform Integration.

Solutions offered by SAP BTP range from Conversation Artificial Intelligence for smart Chat Bots, Intelligent Robotic Process Automation for automating complex decisions, to SAP Analytics Cloud providing a 4D model of insightful Analytics.

Navigating the Cloud: To enter the cloud-based platform, the key lies in the SAP BTP Cockpit. This web-based interface serves as the gateway to manage, monitor, and administer functionality and applications on SAP BTP. To step into this realm, creating a trial account on SAP Cloud Platform Trial is the initial step.

Diving Deeper into SAP BTP:

As we embark on this journey to unravel the layers of SAP BTP, it’s imperative to delve deeper into the key focus areas that make this platform a game-changer in the SAP ecosystem.

Application Development in the Steampunk Era: At the heart of SAP BTP lies a revolutionary approach to application development. Steampunk encapsulates the Restful Programming Model, a topic we’ll explore in detail in subsequent blogs. This model, coupled with CAP (Cloud Application Programming), propels developers into a realm where creativity and functionality converge seamlessly. The Fiori User Interface adds a touch of sophistication, ensuring that user experiences are not just efficient but also aesthetically pleasing.

Integration Mastery: SAP BTP takes pride in its finely tuned integration capabilities. The platform seamlessly brings together SAP and non-SAP solutions, both on-premise and in the cloud. Picture a well-orchestrated symphony where API Management and Cloud Platform Integration act as conductors, ensuring a harmonious integration experience. This is not just about connecting systems; it’s about creating a symphony of data and processes that resonate throughout the enterprise landscape.

Solutions Tailored to Your Needs: SAP BTP doesn’t just stop at development and integration; it offers a diverse array of solutions catering to the evolving needs of businesses. Imagine deploying smart Chat Bots effortlessly with Conversation Artificial Intelligence, automating intricate decisions with Intelligent Robotic Process Automation, or gaining a 4D model of analytics brilliance through SAP Analytics Cloud. These solutions aren’t just features; they are strategic assets that empower businesses to stay ahead in the ever-evolving digital landscape.

The SAP BTP Cockpit: Now, let’s talk about the portal that opens the door to this dynamic world—the SAP BTP Cockpit. This web-based interface serves as the nerve center, allowing users to manage, monitor, and administer functionalities and applications seamlessly. To embark on your journey into the cloud, creating a trial account on SAP Cloud Platform Trial is your passport. The cockpit is more than a dashboard; it’s your command center in the cloud, where you orchestrate your SAP BTP experience.

Looking Ahead: This introductory glimpse into SAP BTP is just the tip of the iceberg. Our upcoming series at ZAPYard will venture into the intricacies of Restful Programming, CAP, Fiori, and more. We’ll guide you through the SAP BTP landscape, ensuring you not only understand its features but also harness its full potential.

| What is BTP in s4 Hana? |

Conclusion: As the curtains rise on SAP BTP, it’s evident that this platform isn’t just a technological shift; it’s a paradigm shift. The fusion of innovation, integration, and tailored solutions positions SAP BTP as a cornerstone in the digital transformation journey. Stay tuned for a series that goes beyond the surface, exploring the nuances that make SAP BTP a force to be reckoned with in the ever-evolving world of enterprise technology. Welcome to a future where SAP BTP isn’t just a platform; it’s an experience.

FAQs

1. What is SAP BTP, and how does it differ from SAP Cloud Platform?

SAP BTP, or Business Technology Platform, is essentially a rebranding of SAP Cloud Platform introduced in 2020. The shift signifies a broader approach, encompassing application development, integration, and a diverse set of solutions. While SAP Cloud Platform primarily focused on cloud services, SAP BTP extends its scope to cater to a more comprehensive set of business technology needs.

2. What is the significance of the term “Steampunk” in SAP BTP?

“Steampunk” in SAP BTP refers specifically to the ABAP Environment within the platform. Derived from retrofuturistic science fiction, the term symbolizes the Power of Steam. In practical terms, Steampunk is geared towards empowering ABAP Developers, providing them with a robust environment for creative and innovative programming.

3. What are the main components of SAP BTP, and how do they benefit businesses?

SAP BTP comprises Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). IaaS eliminates concerns about infrastructure management, PaaS provides a platform for customized solutions, and SaaS offers on-demand cloud-based applications. Together, these components provide businesses with cost efficiency, scalability, and optimal maintenance, fostering innovation and growth.

4. How does SAP BTP support application development, and what is the Restful Programming Model? Application development in SAP BTP is centered around the Steampunk environment. The Restful Programming Model, a key element, will be explored in detail in upcoming blogs. It is a modern approach that simplifies development by focusing on creating APIs with a clear, consistent structure. This model, coupled with Cloud Application Programming (CAP) and Fiori as the User Interface, enhances the developer experience and ensures efficient applications.

5. How can one access SAP BTP, and what is the role of the SAP BTP Cockpit?

Accessing SAP BTP involves creating a trial account on SAP Cloud Platform Trial. The SAP BTP Cockpit serves as the web-based interface, acting as a command center for managing, monitoring, and administering functionalities and applications on the platform. It is the gateway to the cloud experience, providing users with a seamless and intuitive way to navigate and orchestrate their SAP BTP journey.

Accounting -> Financial Accounting -> General Ledger -> Information System-> Balance Sheet

or

Accounting -> Financial accounting -> General ledger -> Information system -> General LedgerReports -> Balance Sheet/Profit and Loss Statement/Cash Flow -> General -> Actual/Actual Comparisons -> Balance Sheet/P+L – F.01

Accounting -> Financial accounting -> General ledger -> Information system -> General LedgerReports -> Balance Sheet/Profit and Loss Statement/Cash Flow -> General – Various

4. Complete a Profit and Loss Report for the Cost of Sales.

A US-based company with 4,000 employees found itself under a soft audit by Oracle for Java Audit license compliance.

Initially presented with a 3-year agreement costing $1.5 million, the company sought external expertise to explore potential alternatives to simply signing the contract.

In their eyes, they had tried to negotiate with Oracle alone for months and were reaching out to Redress and asking, “Is there anything to do? or should we just accept and sign the offer?”

The Process

The situation was thoroughly reviewed, including an analysis of emails and deployment data.

A workshop was hosted to explore all possible options.

Following our advice, the CIO negotiated, rejecting Oracle’s initial demand. The company proposed purchasing licenses only for the specific subset of users who required Java.

Six weeks later, Oracle returned with an offer reduced to 95% of their original “final” offer, leading to a savings of $1.425 million for the client.

A Quote from the CIO

“We felt cornered by Oracle’s compliance claims and the threat of legal action. Reaching out to Redress Compliance, we were guided through our options and gained a clear understanding of our contractual rights. Their negotiation strategy was instrumental, crafting communications that ultimately led to an offer of just $75k, freeing us from any risk posed by Oracle.”

The Solution

Faced with a final offer from Oracle, which was at 1,5m $. Redress supported by:

Develop a response strategy to Oracle’s audit demands.

Formulate a negotiation strategy and provide strategic advice.

Behind-the-scenes negotiation support.

The Outcome

95% reduction from what the client believed was Oracle’s best and final offer.

Need Expert Help?

Is your organization facing Java licensing issues?

Contact us to understand how we can support you and help you avoid paying large sums of money to Oracle.

AI improves facial recognition through machine learning and deep learning.

It’s used in security, consumer electronics, healthcare, and marketing.

Raises ethical concerns regarding privacy, consent, and bias.

Future advancements aim for greater accuracy and inclusivity.

Potential societal impacts include enhanced security, personalized services, and privacy challenges.

Ethical use and regulation are crucial for balancing benefits and individual rights.

The Fundamentals of AI-Powered Facial Recognition

Facial recognition technology leverages AI to identify or verify a person’s identity using their facial features.

This process involves several sophisticated components and methodologies that distinguish AI-powered systems from their traditional counterparts.

How AI Enhances Facial Recognition Technology

AI enhances facial recognition by improving its accuracy, speed, and efficiency. By analyzing vast datasets,

AI algorithms can learn to accurately identify facial features and expressions, even in varying lighting conditions or when the face is partially obscured.

Key Components of AI in Facial Recognition

Machine Learning: Algorithms that enable the system to learn from and adapt to new information without being explicitly programmed.

Neural Networks: Mimic the human brain’s architecture and processing, crucial for recognizing patterns in facial features.

Deep Learning is a subset of machine learning that uses neural networks with many layers, allowing for the automatic extraction of complex features from images.

Comparison with Traditional Facial Recognition Methods

Traditional facial recognition methods rely on more straightforward, rule-based algorithms and are less capable of handling the nuances of human faces.

In contrast, AI-powered systems can continuously learn and improve, making them far more effective in real-world scenarios.

Applications of AI in Facial Recognition

The applications of AI in facial recognition are vast and varied, impacting several industries by offering enhanced capabilities for identity verification, security, and personalized experiences.

Security and Surveillance

In public safety and security operations, AI-powered facial recognition offers a powerful tool for identifying suspects, enhancing surveillance systems, and protecting assets. I

its ability to quickly match faces from video feeds against databases has made it invaluable for law enforcement and security professionals.

Consumer Electronics

AI facial recognition has become a staple in consumer electronics, particularly smartphones and home security systems.

It offers a secure and convenient method for device authentication, leveraging AI to ensure that facial recognition remains accurate and fast.

Healthcare

Within healthcare, facial recognition powered by AI is used for patient identification and monitoring, helping to prevent errors and enhance patient care.

This technology can also assist in identifying patients with certain conditions through facial cues, supporting early diagnosis and treatment strategies.

Retail and Marketing

Retail and marketing sectors are harnessing AI facial recognition to create personalized customer experiences. By identifying customers and improving satisfaction and loyalty, businesses can tailor marketing efforts, recommend products, and enhance customer service.

AI’s integration into facial recognition technology marks a significant leap forward in its development and application.

Offering enhanced accuracy, broader learning capabilities, and diverse applications, AI-powered facial recognition is set to continue expanding across various industries, reshaping how we think about and interact with technology.

Ethical and Privacy Considerations in AI-Powered Facial Recognition

The integration of AI in facial recognition raises critical ethical and privacy considerations that demand attention.

As we navigate these advancements, it’s essential to weigh the benefits against the potential risks to individual rights.

Balancing Security with Individual Rights

Using AI in facial recognition for security purposes presents a delicate balance.

On the one hand, it significantly bolsters public safety and security operations; on the other, it raises concerns about individual privacy and the potential for intrusive surveillance.

Ethical Concerns: Consent, Bias, and Fairness

Consent: The collection and use of facial data often occur without explicit consent from individuals, leading to debates on autonomy and privacy.

Bias and Fairness: AI systems can inherit biases from their training data, resulting in unfair treatment of certain groups. Ensuring fairness in AI algorithms is a paramount challenge that developers face.

Regulatory Landscape: Legal frameworks like the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) aim to protect individuals’ data and privacy. These regulations mandate transparency, consent, and data protection measures for companies using facial recognition technologies.

The dialogue around the ethical use of AI in facial recognition is ongoing. A consensus is leaning towards establishing more robust guidelines and standards to safeguard individual privacy and ensure fairness.

Technological Advancements and Challenges in AI-Powered Facial Recognition

AI has propelled facial recognition technology forward, making it more accurate and adaptable.

However, this progress comes with challenges that researchers and developers work tirelessly to overcome.

Recent Breakthroughs

Advancements in machine learning, neural networks, and deep learning have significantly improved the accuracy and efficiency of facial recognition technology.

These breakthroughs allow real-time identification and verification, even in varied environmental conditions.

Facing the Challenges

Accuracy: Despite improvements, AI-powered facial recognition still struggles with accuracy, especially in low-light conditions or with obscured faces.

Environmental Conditions: Factors like lighting, angles, and obstructions can affect the performance of facial recognition systems, posing challenges in real-world applications.

Ethical Dilemmas: Using AI in facial recognition raises ethical questions regarding privacy, consent, and bias. Addressing these concerns is crucial for the responsible development and deployment of the technology.

Overcoming Obstacles

Ongoing research and development are focused on enhancing AI’s accuracy, reliability, and ethical alignment in facial recognition.

Efforts include creating more diverse datasets to reduce bias, developing algorithms adapting to various environmental conditions, and ensuring compliance with legal and ethical standards.

The future of AI-powered facial recognition is bright, with potential for significant positive impact across numerous sectors.

However, the path forward requires a careful approach that balances innovation with ethical responsibility and respect for privacy.

Future Directions and Potential of AI in Facial Recognition

The trajectory of AI in facial recognition technology points towards a future where its capabilities are more refined and more seamlessly integrated into our daily lives.

As we peer into what lies ahead, it’s evident that AI’s evolving capabilities will unlock new applications, presenting both opportunities and challenges for society.

Evolving Capabilities

The future of AI in facial recognition is marked by continuous improvement in speed, accuracy, and adaptability.

Advanced algorithms will likely overcome limitations, such as recognition in varying light conditions or angles, making the technology more reliable in diverse settings.

Moreover, as AI systems learn from broader datasets, they will become more inclusive, reducing bias and increasing fairness in recognition practices.

Emerging Applications

Crime Prevention: Enhanced AI capabilities in facial recognition are set to play a pivotal role in public safety, aiding law enforcement in identifying and apprehending suspects more efficiently.

Personalized Experiences: In retail and marketing, facial recognition can offer highly personalized shopping experiences, tailoring recommendations and services to individual preferences and behaviors.

Healthcare Advancements: Beyond patient identification, future applications could include monitoring emotional well-being or diagnosing conditions through facial cues, offering new avenues in personalized medicine.

The Potential Impact on Society

As AI-powered facial recognition technology advances, its impact on society is twofold. On the one hand, it promises enhanced security, convenience, and personalization, potentially making our social interactions and daily transactions smoother and more secure.

On the other hand, the widespread adoption of facial recognition raises profound questions about privacy and the nature of public spaces.

It necessitates a societal dialogue on the values we wish to uphold and the kind of technological future we envision.

The key to navigating these future directions lies in striking a balance between leveraging AI’s benefits in facial recognition and safeguarding individual rights and freedoms.

Ethical guidelines, transparent practices, and inclusive policies will be essential in shaping a future where facial recognition technology serves the greater good, enhancing our lives while respecting our privacy and dignity.

Top 10 Real Use Cases for AI in Facial Recognition Technology

Facial recognition technology, powered by artificial intelligence (AI), is reshaping various industries by offering innovative solutions to complex challenges.

Below are ten pivotal use cases demonstrating its versatility and impact.

1. Security and Surveillance

Industry: Public Safety, Law Enforcement

Benefits: Enhances security measures by identifying suspects and individuals of interest in real time.

Technology: Real-time facial recognition integrated with surveillance cameras.

2. Smartphone Authentication

Industry: Consumer Electronics

Benefits: Provides a secure and convenient way for users to unlock their devices.

Technology: AI algorithms that analyze facial features to verify the user’s identity.

3. Airport Check-ins and Border Control

Industry: Travel and Immigration

Benefits: Streamlines check-in and enhances border security by quickly verifying identities.

Technology: Advanced facial recognition systems can efficiently process vast numbers of passengers.

4. Personalized Retail Experience

Industry: Retail

Benefits: Offers tailored shopping experiences by recognizing returning customers and suggesting products based on previous purchases.

Technology: In-store cameras with facial recognition software match faces with customer profiles.

5. Healthcare Patient Management

Industry: Healthcare

Benefits: Improves patient care by accurately identifying patients and accessing their medical records swiftly.

Technology: Facial recognition systems integrated with hospital databases.

Benefits: Enhances security for banking transactions by using facial recognition for authentication in ATMs and online banking.

Technology: Secure facial recognition algorithms that work with ATMs and banking apps.

7. Attendance Tracking in Education and Workplaces

Industry: Education, Corporate

Benefits: Automates attendance tracking, saving time and reducing fraud.

Technology: AI-powered systems that recognize students’ or employees’ faces to record attendance.

8. Public Health Monitoring

Industry: Public Health, Law Enforcement

Benefits: Monitors compliance with public health directives, such as mask-wearing or quarantine enforcement.

Technology: Facial recognition software that can identify faces even with masks on.

9. Access Control in Secure Facilities

Industry: Corporate, Government

Benefits: Enhances security by restricting access to sensitive areas based on facial identity.

Technology: Integrated facial recognition systems at entry points to verify identities against an authorized database.

10. Personalized Marketing and Advertising

Industry: Marketing and Advertising

Benefits: Delivers personalized advertising content by recognizing demographic features or specific individuals.

Technology: Digital signage and online platforms equipped with facial recognition to tailor marketing messages.

These use cases illustrate the broad spectrum of applications for AI in facial recognition technology, highlighting its potential to revolutionize security, convenience, and personalization across multiple industries.

As technology advances, these applications are set to become even more integrated into our daily lives, underscoring the importance of addressing the ethical and privacy considerations associated with their use.

FAQs

How does AI improve facial recognition?

AI enhances facial recognition by employing machine and deep learning, allowing systems to learn and improve from vast amounts of data.

Where is AI-powered facial recognition used?

This technology is utilized across various sectors, including security, consumer electronics, healthcare, and marketing for various applications.

What are the ethical concerns with AI facial recognition?

Key ethical issues include privacy invasion, lack of consent from recognized individuals, and algorithmic bias that could lead to unfair treatment.

How do future advancements in AI facial recognition look?

Future developments aim to increase the accuracy and inclusivity of facial recognition, making it more reliable across diverse populations and conditions.

What societal impacts does AI facial recognition have?

While it can enhance security and provide personalized services, it also poses significant privacy challenges and questions around surveillance.

Why is ethical use and regulation important for facial recognition?

Balancing the benefits of facial recognition with individual rights necessitates ethical guidelines and strict regulations to prevent misuse.

Can AI facial recognition be biased?

If the training data is not diverse, AI systems can develop biases, leading to unequal or unfair recognition outcomes.

What steps are being taken to ensure privacy in AI facial recognition?

Developers and regulators are working on privacy-preserving technologies and strict data-handling policies to protect individuals’ information.

How can consumers protect themselves against facial recognition?

Being informed about where and how facial recognition technology is used and understanding consent options are crucial for individual protection.

Is facial recognition always accurate?

While highly effective, facial recognition can sometimes be inaccurate, especially in challenging conditions or with low-quality images.

How are biases in facial recognition addressed?

Efforts include using more diverse datasets for training and applying algorithmic fairness approaches to reduce biases.

What future applications might emerge from AI in facial recognition?

Potential applications include more sophisticated security systems, advanced health monitoring, and immersive augmented reality experiences.

How is facial recognition regulated?

Laws such as GDPR in Europe and CCPA in California set standards for consent, data protection, and individual rights regarding facial data.

Can facial recognition technology recognize emotions?

Emerging AI models are being developed to recognize emotional expressions, though this area is still in the early stages of research.

What role do consumers play in the development of facial recognition?

Consumer feedback, demand for privacy, and ethical considerations can drive companies to adopt responsible development practices for facial recognition technologies.